- The Paradox: High Belief, Low Action — What the Data Actually Shows

- The Real Barrier Isn’t Skepticism, It’s Integration — Unpacking the 54% Finding

- What Integration Difficulty Actually Looks Like on the Ground

- Why the Other Barriers Are Smaller Than You’d Expect

- The Same Pattern Appears in External Barriers

- Why Larger Organizations Feel This Most Acutely

- The Cost of Waiting: Why Senior Leaders and Big Spenders Feel the Urgency More

- What Crossing the Adoption Threshold Looks Like in Practice

- Mapping Workflows Before Adoption, Not After

- Building Measurement Infrastructure in Advance

- Starting With Contained Pilots

- Closing Thought: The Barrier Is Real, but It’s Operational, Not Philosophical

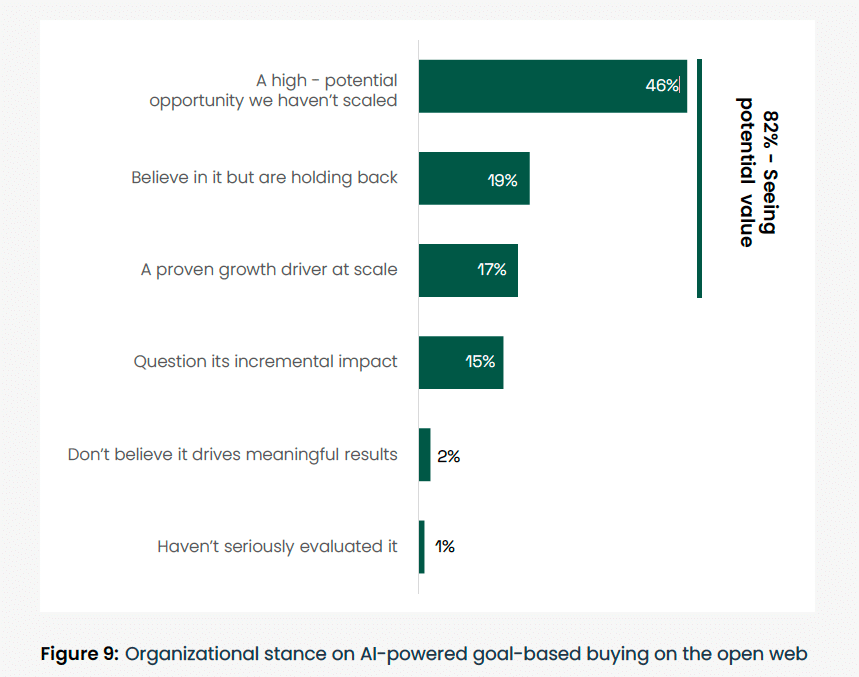

An overwhelming 82% percent of marketers say agentic AI on the open web represents a real growth opportunity, but most still aren’t using it. That gap isn’t a fluke, it’s where the industry stands right now: strong belief, slow action, and a growing divide between the companies experimenting early and the ones waiting on the sidelines.

The hesitation is understandable. Agentic AI is moving fast, and many teams are still trying to figure out where the technology fits into existing workflows, budgets, and measurement models. But, while others debate the timing, early adopters are already learning what works, refining their strategies, and building advantages that won’t be easy to catch up to later.

The Agentic Advantage in Performance Marketing Report 2026

The Paradox: High Belief, Low Action — What the Data Actually Shows

In performance marketing, 82% agreement on anything is rare. This is an industry built on skepticism, where marketers learn to question vendor claims, inflated projections, and “next big thing” narratives. Getting four out of five professionals to agree on a growth opportunity almost never happens unless the results already feel undeniable.

Interestingly, in this case, the results aren’t fully proven yet. Not at scale, anyway. That’s what makes the data so unusual: most of the marketers who believe in agentic AI haven’t actually acted on that belief. They aren’t testing the channel and walking away disappointed, they aren’t running pilots that failed to perform. Instead, many are stuck in a middle ground: convinced of the opportunity, but slow to operationalize it.

That distinction matters. From the outside, hesitation and disbelief can look identical. In practice, they’re completely different market signals. A skeptical market has already decided something won’t work. A hesitant market believes it probably will, but hasn’t acted yet.

The survey data points clearly toward hesitation, not rejection. Marketers aren’t dismissing the channel — they’re waiting, evaluating, delaying rollout, or struggling to determine how it fits into existing systems and priorities. All of which raises a more interesting question: Why has a near-consensus belief, in an industry that rarely agrees on anything, produced so little action so far?

Where the Market Actually Stands

The survey breaks that 82% agreement into three distinct groups, each representing a different stage of open web advertising adoption:

- The Untapped Potential (46%): Nearly half of marketers see agentic AI as a meaningful growth opportunity, but have yet to act on it at scale.

- The Hesitant Believers (19%): This group recognizes the value, but is waiting for the right solutions or internal conditions to align.

- The Early Scalers (17%): These marketers already treat open web campaigns as a proven growth driver and run them at scale.

What’s striking is how small the skeptical segment actually is. Only about 15% question whether the incremental impact is real, while just 3% are openly dismissive or haven’t seriously evaluated the category at all.

Again, that means 82% of the market falls on the believing side of the equation. Just 18% remain skeptical or unevaluated, and even within that group, most aren’t rejecting the technology outright. Many are simply unconvinced about one or two aspects of its effectiveness.

In other words, belief isn’t the barrier. The real disconnect is between conviction and execution. That, in turn, raises a bigger question that the survey can’t fully answer on its own: If so many organizations already believe the opportunity is real, why are scaled adoption rates so low?

The Real Barrier Isn’t Skepticism, It’s Integration — Unpacking the 54% Finding

The biggest obstacle to adoption isn’t doubt. It’s operations.

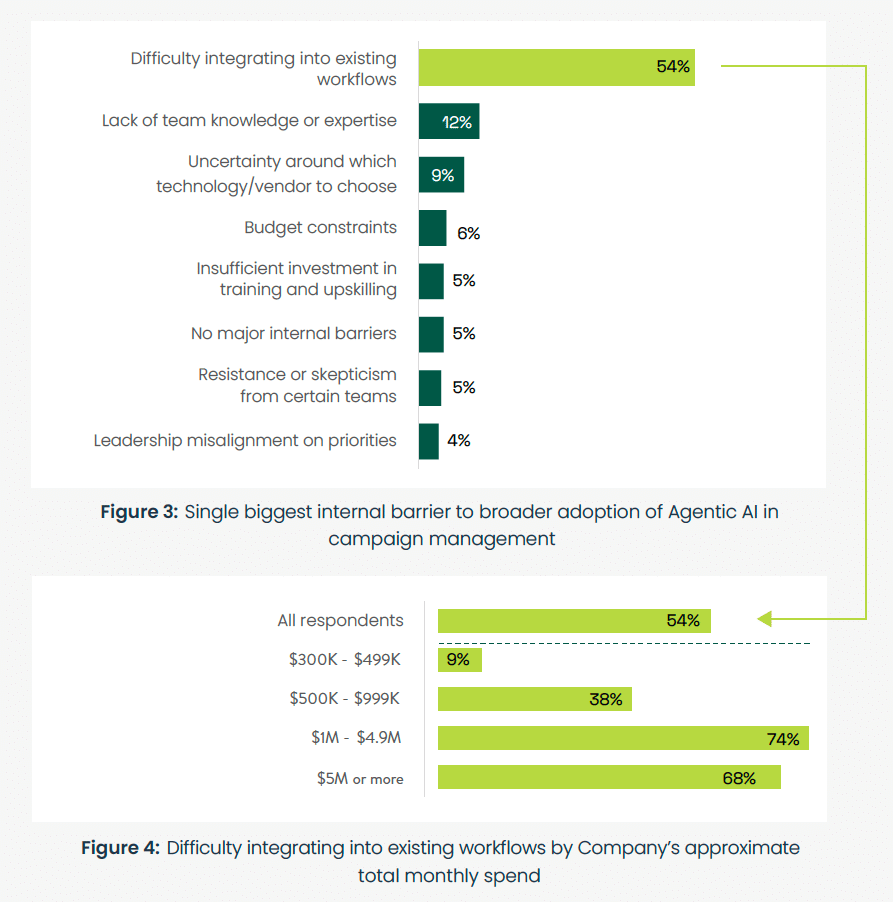

When marketers were asked to identify the single largest internal barrier to adopting agentic AI, more than half pointed to one issue: integrating it into existing workflows. No other challenge came close. Among all performance marketing barriers surfaced in the survey, marketing technology integration stood out as the dominant friction point.

Here’s how the responses broke down:

- Difficulty integrating into existing workflows: 54%.

- Lack of team knowledge or expertise: 12%.

- Uncertainty about which technology or vendor to choose: 9%.

- Budget constraints: 6%.

- Insufficient investment in training and upskilling: 5%.

- No major internal barriers: 5%.

- Resistance or skepticism from certain teams: 5%.

- Leadership misalignment on priorities: 4%.

The data is hard to ignore.

The industry isn’t being held back by budget concerns. It isn’t even stalled by skepticism about whether the technology works. The dominant challenge is far more practical: figuring out how an autonomous system fits into a marketing infrastructure that was never designed for it.

Agentic AI doesn’t operate in isolation. It has to connect to existing tech stacks, attribution models, approval processes, reporting systems, and cross-functional workflows that are already deeply embedded inside organizations. In many cases, the companies that stand to benefit the most are also the ones dealing with the highest operational complexity.

That tension shows up clearly in the data. The hesitation isn’t necessarily a sign that organizations are falling behind. In many cases, it’s the natural result of trying to integrate a functionally new operating model into systems built for a very different era of marketing.

What Integration Difficulty Actually Looks Like on the Ground

Imagine a senior media buyer managing $2 million a month across paid channels. That budget already runs through a carefully built system — vendor relationships, attribution logic, reporting cadences, approval workflows, and budget authorization processes that have evolved together over the years.

In that environment, adopting an autonomous platform isn’t as simple as adding another tool to the stack. It changes how the system itself operates. Marketing technology integration at this level forces teams to rethink questions like:

- Where does an autonomous platform fit alongside existing vendors and channel partners?

- How do you measure attribution when the system is making its own optimization decisions in real time?

- What happens to reporting workflows that were designed around human-led campaign management?

- How do creative approval processes adapt when campaigns move faster than traditional review cycles?

- What does budget authorization look like when a machine is continuously allocating spend on its own?

None of these problems are impossible to solve, but none of them are minor, either. That’s what makes the 54% figure so important: it’s not a vague objection or a sign of organizational laziness, it’s a reflection of how modern marketing operations are actually built.

The gap between belief and adoption doesn’t exist because marketers fail to see the opportunity. It exists because integrating a fundamentally different operating model into an already complex system is difficult, time-consuming, and organizationally disruptive — even for teams that believe the payoff is worth it.

Why the Other Barriers Are Smaller Than You’d Expect

The smaller performance marketing barriers in the survey data are revealing in their own right:

- Budget constraints (6%) suggest that most organizations have already concluded that the investment is financially justifiable. The issue isn’t whether they can spend the money, it’s whether they can operationalize the technology effectively once they do.

- Vendor uncertainty (9%) points to a market that’s already maturing. Buyers may not agree on the best partner, but most no longer seem confused about whether credible options exist.

- Team knowledge gaps (12%) are real, but they’re also manageable. Training teams and building expertise takes time, yet even that challenge ranks far below the complexity of integration itself.

The data tells a clear story, that the industry has long moved past the upstream questions. Should we be doing this? Most marketers think yes. Can we afford it? Again, mostly yes. Are there legitimate vendors in the space? For the most part, yes.

What remains is the harder question, and it’s one that slows adoption even after belief is established. How do you integrate an autonomous system into the way the organization already works today?

The Same Pattern Appears in External Barriers

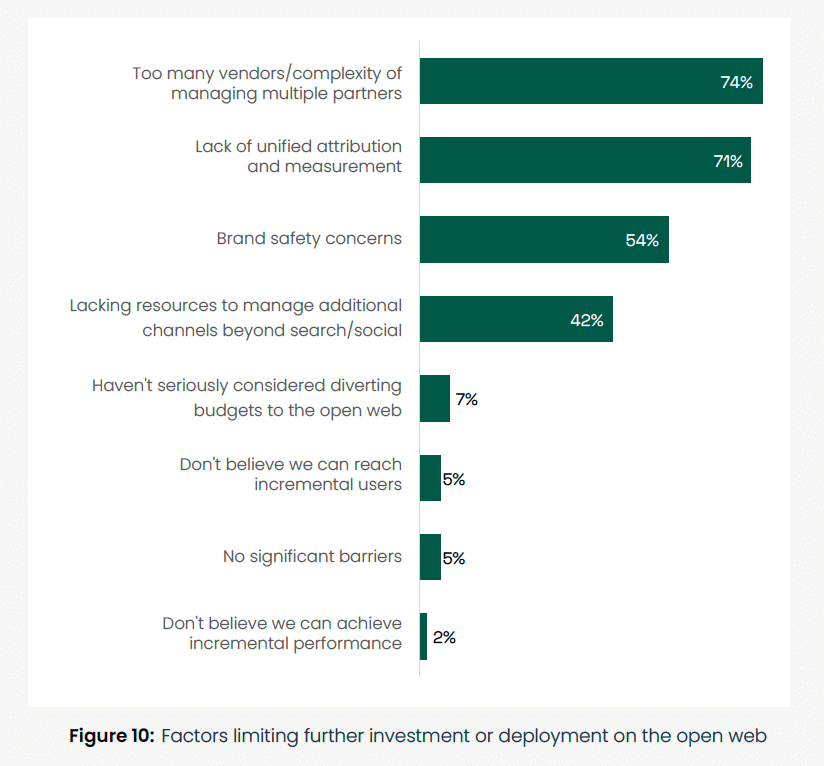

The operational bottlenecks don’t stop at internal workflows. When marketers were asked what has limited additional investment in open web advertising channels specifically, the responses followed a similar pattern:

- 74% cited the complexity of managing too many vendors and partners.

- 71% pointed to the lack of unified attribution and measurement.

- 54% raised brand safety concerns.

- 42% said they lacked the resources to manage additional channels effectively.

Meanwhile, outright skepticism barely registered. Only 5% said they don’t believe the channel can reach incremental users. Just 2% said they don’t believe incremental performance is achievable at all.

Once again, the market isn’t signaling a lack of confidence in the opportunity itself, it’s signaling friction in the systems required to support it. Marketers largely believe the performance upside exists. What they’re struggling with is the complexity that comes with adding another layer of vendors, measurement frameworks, governance, and channel management into already crowded marketing ecosystems.

Why Larger Organizations Feel This Most Acutely

The integration challenge isn’t evenly distributed across the market. In fact, it scales almost directly alongside monthly budget size. When asked to identify their primary obstacle, the percentage of organizations pointing to integration grows significantly as spend increases:

- $300K–$499K budget: 9%.

- $500K–$999K budget: 38%.

- $1M–$4.9M budget: 74%.

- $5M+ budget: 68%.

At first glance, that seems backward. Larger organizations typically have more resources, more robust teams, stronger technical infrastructure, and more specialized expertise. In theory, they should be better positioned to absorb a new system than smaller, leaner companies, but the data points in the other direction.

The reason is fairly straightforward: Complex systems are harder to change than simpler ones. As organizations scale, so does the complexity surrounding every operational decision:

- More infrastructure creates more integration points.

- More legacy systems create more dependencies and workarounds.

- More stakeholders introduce more competing priorities and approval layers.

- More established performance creates greater risk if implementation goes poorly.

In other words, the very sophistication that made these organizations successful is also what makes transformations more difficult. These companies aren’t starting from scratch: they’ve spent years building performance engines, attribution frameworks, reporting structure, vendor ecosystems, and cross-functional operating rhythms that already work at scale. Integrating a new autonomous system into that environment is inherently more complicated than adding it to a smaller, less mature operation.

That complexity shouldn’t be mistaken for resistance or failure. It’s a predictable consequence of scale. But, it also means the pressure to solve the integration problem is greatest where the opportunity is largest. The organizations managing the biggest budgets have the most to gain from successful adoption — and potentially the most to lose if they fall behind when competitors figure it out first.

The Cost of Waiting: Why Senior Leaders and Big Spenders Feel the Urgency More

The integration barrier helps explain why many organizations haven’t moved yet, but the survey reveals something equally important: The cost of waiting isn’t distributed evenly. It falls hardest on the leaders managing the largest budgets.

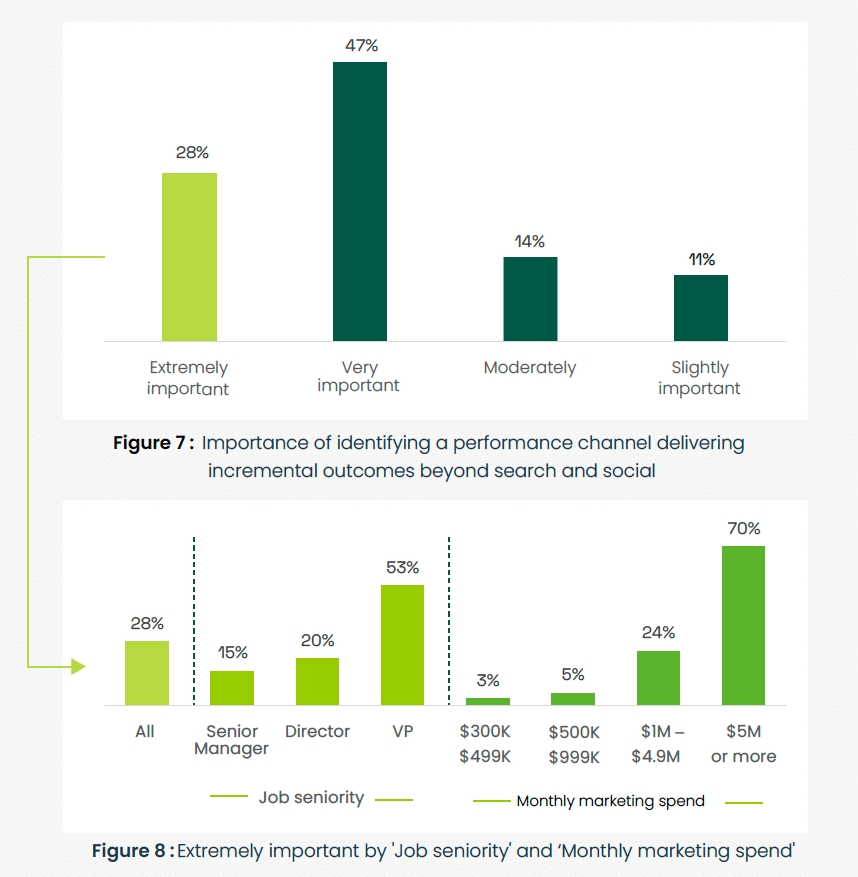

Overall, 75% of marketing leaders say finding an incremental performance channel beyond search and social is very or extremely important, but the urgency becomes much clearer when the data is segmented by seniority.

Of senior management weighing in, the following percentage rated it as “extremely important”:

- 53% of VPs.

- 20% of Directors.

- 15% of Senior Managers.

The same pattern appears when segmented by monthly spend, showing a dramatic escalation in urgency:

- 3% of $300K–$499K spenders.

- 5% of $500K–$999K spenders.

- 24% of $1M–$4.9M spenders.

- 70% of $5M+ spenders.

That sharp jump at the highest spending tier is revealing. The people managing the biggest budgets are also the people seeing diminishing marginal returns most clearly. When an organization is spending millions each month across search and social, the effects of saturation become impossible to ignore. Every additional dollar works a little less efficiently than the one before it. At that scale, finding a new source of incremental growth becomes a financial necessity.

The organizations feeling the greatest urgency are also the organizations with the most capital available to reallocate once operational barriers are solved. The budgets already exist. The intent already exists. What’s missing is the ability to integrate and scale confidently.

That’s where the competitive advantage begins to form. The first-mover advantage in agentic AI on the open web isn’t theoretical. It shows up in budget share, learning curves, operational maturity, and performance efficiency, and it will likely flow to the organizations that solve the integration challenge before everyone else does.

The Diminishing Returns Problem Nobody Talks About

When a company spends tens of millions of dollars a year on paid search and paid social, diminishing returns stop being theoretical. They become a reality. At a certain scale, every additional dollar produces less incremental impact than the one before it. That’s the underlying force driving much of the urgency in the survey data.

The mechanics are familiar to anyone managing large performance budgets:

- High-intent audiences have already been reached: The customers most likely to convert are already seeing your ads — often alongside competitors targeting the same users.

- Ad fatigue compounds over time: Repeated exposure to the same creative naturally reduces responsiveness.

- CPAs begin to rise: As the most efficient inventory becomes more competitive, incremental conversions get more expensive.

- Auction pressure intensifies: More advertisers compete for the same keywords, audiences, and placements, pushing costs higher across the board.

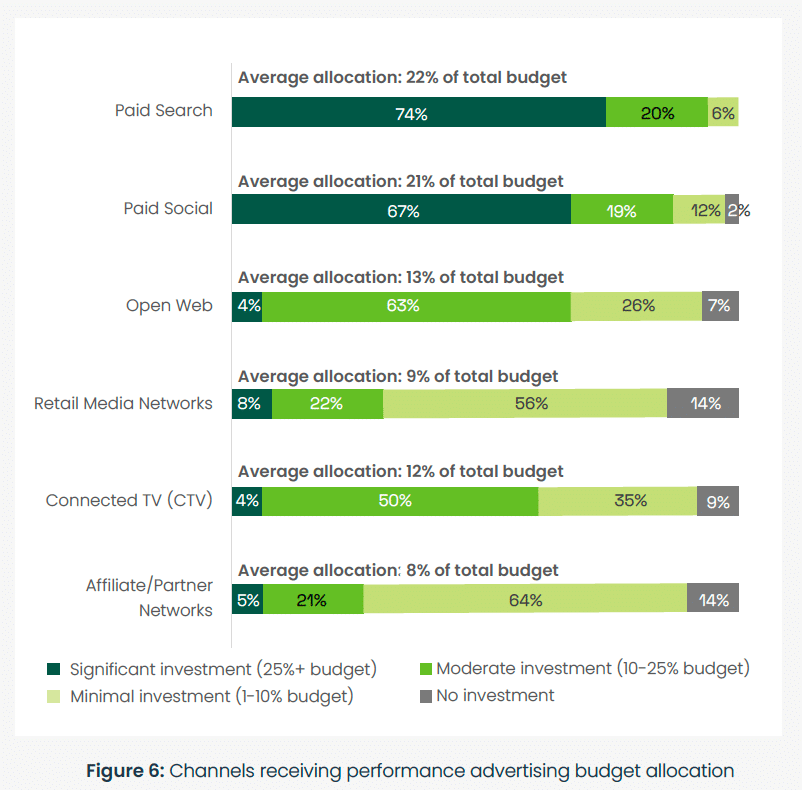

The data reveals a heavy reliance on these saturated channels:

- 74% of respondents allocate at least 25% of their performance budget to paid search.

- 67% do the same with paid social.

These channels still drive enormous value, but they’re also where the limits of scale become most visible, especially to the executives closest to the numbers. For a senior leader overseeing a $5-million-per-month performance program, saturation isn’t an abstract economic concept. It’s the day-to-day experience of watching marginal returns flatten across the two channels consuming the majority of the budget. Once that happens, finding a new source of incremental performance stops being optional.

What Crossing the Adoption Threshold Looks Like in Practice

The 17% of organizations already running open web performance campaigns at scale didn’t get there by waiting for the integration problem to solve itself. They got there by treating agentic AI adoption as an operational transformation, rather than a technology purchase.

If the barrier is operational, the solution has to be operational, too. In practice, that usually comes down to three disciplines the rest of the market is still working through.

Mapping Workflows Before Adoption, Not After

The fastest-moving teams identify the friction points early. Before contracts are signed or pilots begin, they already understand which approval chains, reporting cadences, attribution models, and decision-making processes will need to evolve. That work happens up front, not reactively in the middle of implementation.

Building Measurement Infrastructure in Advance

One of the fastest ways for a pilot to stall is trying to measure incremental impact using a framework that was never designed for autonomous optimization in the first place. Organizations that scale successfully tend to establish their measurement logic early, so the system’s contribution can be evaluated from the start instead of debated later.

Starting With Contained Pilots

The organizations succeeding in this space rarely try to automate their entire performance operation at once. Instead, they begin with a tightly defined audience, objective, and budget range. That creates room for the operating model to mature in a controlled environment before broader rollout begins.

None of this is especially flashy. In fact, most of it looks like disciplined operational planning — the kind of work that determines whether transformational efforts actually scale. The 17% who have crossed the threshold weren’t necessarily early because they had better technology. They moved first because they treated workflow design, measurement, and organizational alignment as core parts of the adoption process from the beginning.

Closing Thought: The Barrier Is Real, but It’s Operational, Not Philosophical

The 17% already running open web performance campaigns at scale aren’t simply ahead on technology. They’re ahead on the operational learning curve — the part competitors can’t shortcut later by writing a bigger check.

That’s the underappreciated dynamic in the survey data. Belief is no longer a differentiator. Budget isn’t either. What separates the Early Scalers from the Untapped Potential is the willingness to treat workflow design, measurement infrastructure, and organizational alignment as the actual work of adoption, not the prerequisites to it.

At this point, the philosophical debate about whether agentic AI belongs in performance marketing is largely over. Most of the industry has already answered that question for itself. What matters now is execution. Who can integrate the technology effectively? Who can adapt workflows, measurement systems, and reporting structures quickly enough to scale? Who can move from belief to operational maturity before competitors do? Because conviction alone no longer creates an advantage. Execution does.